“Simplified” income sprinkling measures

12 minute read | co-authored by Clayton Achen and Carol Sadler

December 13, 2017: the headline on the Department of Finance’s website reads: “Government Simplifies Measures to Restrict Income Sprinkling”. Well this is welcome news! And just in time for Christmas! Oh… wait a minute, the release includes 24-pages of explanatory notes, 20 ‘real-life’ examples, 14 FAQs, 11-pages of technical amendments, 7-pages of background (and here), 2-weeks for Canadians to prepare, a nation of outraged entrepreneurial families and tax advisers… and a partridge in a pear-tree.

We’ve had lots of time to prepare for this, right? Not quite. On certain items (discussed below) the Finance Minister’s ‘climb-down’ from the July 18th, 2017 tax proposals are welcome, however the December 13 draft legislation is totally new compared to the July 18th, 2017 draft, but is still effective January 1, 2018. Entrepreneurial families and tax advisers have 2-weeks to digest and apply the new, business-altering, legislation; 2-weeks which fall over the 2017 Christmas Holiday Season.

Do I detect a theme, Minister Morneau? Remember that the July 18th proposals allowed a “consultation period” (gawk) which fell mostly over summer holidays and harvest season, and mostly while Parliament was not in session. This time the release comes over the Christmas holidays… while Parliament is not in session. I suppose consistency is important. Obviously, Minister Morneau will be happy to avoid Pierre Poilievre’s questions until January 29, 2018 because Minister Morneau has failed Canada so miserably in Question Period over the last 3 months. Unfortunately for everyone affected, this new “income sprinkling” legislation will come into effect 4-weeks before it can be openly debated in the House of Commons; presuming it passes in the 2018 budget bill.

What does the Standing Senate Committee on National Finance think?

Mere hours before Minister Morneau took to the airwaves to announce the ‘simplified measures’, the Standing Senate Committee on National Finance released its report on the July 18th tax measures (this is a great read). This report is the result of the Senate Committee’s tour of Canada and, unlike the Liberal Government’s process, real engagement and consultation with affected stakeholders. Some highlights:

- “Recommendation 1: That the Minister of Finance withdraw his proposed changes to the Income Tax Act respecting Canadian-controlled private corporations” (that’s right, all of it);

- “Recommendation 2: That the Government of Canada undertake an independent comprehensive review of Canada’s tax system…”;

- Recommendation 3: If anything is to change, wait until 2019;

- “Our committee is deeply concerned about the possible negative effects of the proposed changes on the Canadian economy. They could undermine Canada’s competitiveness, leading to less investment and less employment.”;

- “Much of the outrage and the government’s subsequent amendments to its proposals could have been avoided if it had undertaken thorough, open consultations based upon neutrally stated tax objectives.”;

- “We are not convinced that the government has made a good case for its proposals.”

We have not heard if the Senate intends to block the December 13th legislation because of the Committee’s findings. Some tax experts believe that the Senate lacks the power to block this legislation, while some remain hopeful. I suspect that the Liberal Government will downplay this report and move ahead with its proposed measures.

Income Sprinkling: the new regime

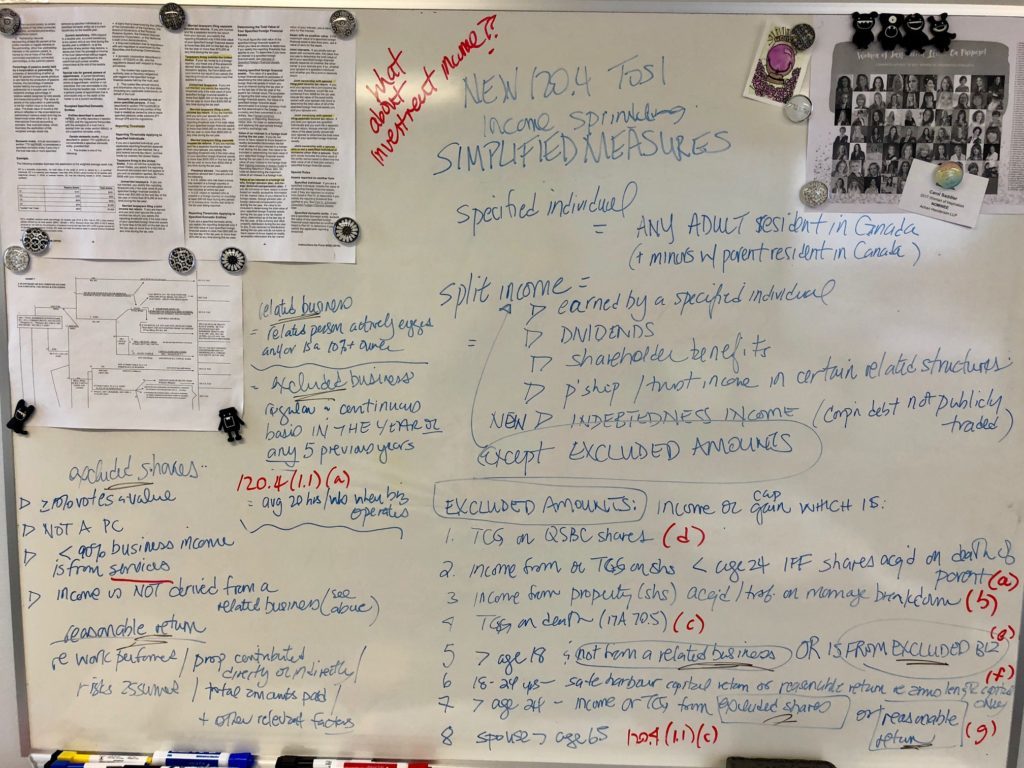

Now that’s out of the way, let’s get into the changes. The overall theme of the ‘income sprinkling’, or Tax on Split Income (“TOSI”), rules is to apply the top personal marginal tax rate on income paid to certain people (defined as “specified individuals”) unless that income is exempted (defined as “excluded amounts”).

What has changed since July 18, 2017?

Finance did, apparently, read a few of the 21,000+ submissions received during its initial ‘consultation period’ as it has carved-out certain scenarios from the July 18thproposals:

- TOSI will not be applied to compound income (income earned from the re-investment of other income which was subject to TOSI). This is great news;

- “Related persons” will not include aunts, uncles, nieces and nephews. “Related persons” will, instead retain its traditional definition and, in this case, will include adult direct descendants and siblings, i.e. grand-parnets, parents, children, grand-children and siblings);

- The revised draft will no longer deem capital gains realized on the transfer of private company shares to related adults to be dividends (the current “Kiddie-Tax” rules on distributions to minors remain unchanged);

- The TOSI rules will not apply to capital gains on the disposition of qualified small business corporation shares, or qualified farm or fishing property;

- The TOSI rules will not apply in the case of property transferred under a separation agreement resulting from a marriage breakdown;

- The TOSI rules will not apply to taxable capital gains triggered on the death of a taxpayer.

When am I subject to the new ‘income sprinkling’ rules?

Under the original tax rules, before these proposals, income earned or paid to a minor child from a company in which a parent held at least a 10% interest, was “split income” and was TOSI (taxed at the highest marginal rate). This remains unchanged.

Under the original tax rules, before these proposals, income earned or paid to a minor child from a company in which a parent held at least a 10% interest, was “split income” and was TOSI (taxed at the highest marginal rate). This remains unchanged.

The current proposals re-introduce TOSI to adults, in a somewhat more comprehensible form than the July 18th, 2017 proposals did. Effective January 1, 2018, if you own shares of a Canadian Controlled Private Corporation (“CCPC”) and you are related to a person (see above) who owns 10% or more of that same company (including yourself, by the way… so you are caught if you own more than 10% of a private company – you’re welcome), you a “Specified Individual” and income you receive from that company is subject to the TOSI rules and the top marginal tax rate.

What income is not subject to the income sprinkling (TOSI) rules?

When the income is an “excluded amount”. Simply put, income which qualifies for one of the exceptions below is not subject to these new rules and can be paid to / received by an individual without attracting the highest marginal tax rate. The proposals list five categories of “excluded amounts”, which depend on the age of the individual receiving the dividend as well as the details of that income. Specific limitations apply to those ages 18 – 24. Please note that Salaries are already subject to their own ‘reasonability tests’ so when you see the word ‘income’ below, think dividends and interest.

The five categories are:

- Individuals 18 or older: If the income is from an “excluded business”, meaning one in which the individual is actively engaged on a regular, continuous and substantial basis, at least 20 hours per week, in either the current year OR any five past years (not necessarily consecutive). Interestingly, this ‘excluded business’ exemption can be inherited so if a person qualifies and passes the shares on via inheritance, income to the recipient will continue to be exempted from these rules under the “excluded business” exclusion even if they’re not active in the company’s business;

- Individuals between ages 18-24: If these individuals cannot meet the “excluded business” exemption, they may qualify for the ‘safe harbor capital return’ exemption.Under this exemption, ‘specified individuals’ can receive income calculated at return of no more than the prescribed rate (currently 1%) on the individual’s capital invested. Those aged 18 -24 may also qualify for a “reasonable return” (#4 – below) with respect to capital they invested in the company that was not acquired from a related person and was not financed by a loan or borrowing;

- Individuals > 24 years old: If the income is paid on “excluded shares”, where:

- The individual owns 10% or more of the fair market value and 10% or more of the votes of the CCPC’s issued shares;

- The company is not a professional corporation;

- Less than 90% of the company’s “Business Income” is from the provision of “Services”.

There are a several problems with the concept of “excluded shares”:

- What is “Business income”? What it is not, is a defined term in the income tax act. We do not know what this means;

- Obviously, the Liberal Government does not believe Professional Corporations should split income. We surmise the exclusion of service income is meant to treat all service providers the same, rather than excluding only the small cohort of professional corporations. We believe that excluding all services in favor of goods seems like arbitrary tax policy. What sense is there in tax legislation that favors a bike shop over a yoga studio? In Alberta, this will have a dramatic impact on our Oil and Gas service sector (a major job creator in Canada). Quebec enacted rules based on the number of employees and the same occurs in the Income Tax Act for investment income earned by corporations. The “personal services business” rules also limit certain income-splitting concerns. Frankly, the current tax rules provide us with a more reasonable approach than these new proposals;

- The proposed legislation does not clearly define a ‘service’. For example, what about software sales? What about property leases? Our firm and some of our IT clients resell software and those sales make up at least 10% of their revenues. Can businesses be restructured to ensure they are selling at least 10% ‘goods’ to fit in with this exemption? Can these rules be managed simply by selling a good and giving away the service?;

- The income cannot be derived from a “related business in respect of the specified individual”. Holding companies generally earn their income from related operating companies. Income from a company which may have otherwise qualified for this exemption may not qualify simply because of the design of the corporate structure. There are good (non-tax) business reasons for utilizing a multi-company structure, but absent changes by Finance, distributions from such structures may be subject to TOSI, simply because they are multi-company structures;

- What happens if an individual holds their interest through a discretionary family trust rather than directly? The definition of “excluded shares” requires that shares be “owned by the specified individual”. It is possible that shares owned through a family trust will not qualify as “excluded shares”. Is this Finance’s way of raising the tax rates on trust distributions? Is every corporate structure involving a family trust and an operating company now in need of a reorganization by the end of 2019 in order to be able to pay out income to its shareholders without the application of ‘TOSI’? If so, this is obviously retroactive legislation.

- Individuals> 24 years old: If the income represents a “reasonable return” on capital invested. The “reasonable return” test applies with respect to any or all the following five factors:

- Work by the individual for the business;

- Property contributed in support of the business;

- Risks assumed in respect of the business;

- Amounts already paid to (or for the benefit of) the individual in respect of the business;

- Any other “such other factors as may be relevant” (wow!).

While the last point may leave some creative space for tax professionals to determine other factors which ‘may be relevant’, the burden of interpreting this exemption will ultimately rest with our tax courts, which will take years. Further, we cringe every time we see the word ‘reasonable’ in draft legislation because we perceive this allows the CRA tremendous powers to inflict tremendous pain on small business owners by disagreeing with the interpretation of ‘reasonable’.

- Individual > 64 years old: may split income from his/her private corporation with a spouse. This must be the result of entrepreneur’s objections that pension splitting is available between spouses.

“Gender-Based Analysis”

The following excerpt from the government’s release is, in our view, unfortunate and deserves some attention:

“Data show that men represent over 70% of higher-income earners initiating income sprinkling strategies, and women represent about 68% of recipients of sprinkled dividends (and 58% of recipients of income derived from trust and partnerships). While this income is of benefit for recipients, it also creates incentives that reduce female participation in the workforce. Increased participation of women in the workforce is a source of economic opportunity for individuals and is a major driver of overall economic growth.”

Our firm has a real problem with this statement. The government seems to believe that ‘income sprinkling’ is a main factor for spouses (in this case women) deciding to stay home and raise a family. Our firm’s female partner, Carol Sadler – an entrepreneurial mother, would tell you that the possibility of some tax savings barely factors into these types of decisions. The fact that the government attempts to reduce a spouse’s decision to stay at home (or return to work) to ‘income sprinkling’ is utterly offensive.

Also, is the government suggesting that stay-at-home spouses are bad for the economy? If so, we find this is both short-sighted and a bit stomach turning.

And finally…

There is still significant uncertainty on how these rules should be applied by owners of CCPCs, particularly surrounding the ownership and income tests in the “excluded shares” exception and in what ‘reasonable’ means in the “reasonable return” exception. The CRA has released a number of examples intended to help business owners understand these changes, which is very helpful, however the example set is very incomplete. Also, the CRA’s interpretation of the law does not represent the law itself so the clarification which we, as tax practitioners, seek is still lacking and may have to, ultimately, be delivered by our court system; which amounts to a major flaw in any legislation package.

The United States is about to reduce personal and corporate tax rates, including a drop in the US Federal corporate tax rate to 21% from 35%. We expect their changes could be in place before Christmas 2017. Canadian private company owners are currently faced with a combined top marginal tax rate of more than 50% (dividends), while the US owners’ rate will be in the low-to-mid-40%’s. Canadian public companies and other large private companies, who are major employers may have an opportunity to increase their profit margin by relocating to the United States. This is compounded by other punitive taxes which aren’t in place in the US, such as carbon tax. Ultimately, the US is starting to look a lot better to the difference makers in Canada; this is about to become a real problem for our country.

Lastly, these proposals remain so intensely complex that every paper we have read about this subject since December 13, 2017 seems to have different ideas about how these rules will apply. Every time we re-read this new proposed legislation we think of new flaws and complexities for which there are no apparent answers. This excessive complexity cannot be understated, which is another reason why these changes should not be rushed through by the government. Broad tax reform is clearly needed in Canada, but the Liberal government seems hellbent on continuing to patch the leaky boat with duct tape.

If you want clarification or have questions about how these changes affect you, please do not hesitate to contact your Achen Henderson professional.

Clayton E. Achen

Carol Sadler